INVESTMENTS

Education Secretary Betsy Devos calls student debt forgiveness ‘a truly insidious notion’ and free college ‘a socialist takeover’

Outgoing Education Secretary Betsy DeVos presented a spirited defense of her record after four years and skewered proposals from progressive politicians related to student debt cancellation and free college at the virtual 2020 Federal Student Aid (FSA) Training Conference on Tuesday.

“After nearly four years on the job, I want to take a few moments to reflect on the remarkable transformations that we led at FSA in recent years,” DeVos said at the beginning of the keynote speech, “and then discuss what still needs to be done for students.”

‘A socialist takeover of higher education’

DeVos took aim at proposals to cancel student debt, a proposal that the incoming Biden administration campaigned on, calling debt forgiveness “the truly insidious notion of government gift giving.”

“We’ve heard shrill calls to ‘cancel,’ to ‘forgive,’ to ‘make it all free,’” Devos added. “Any innocuous label out there can’t obfuscate what it really is: wrong.”

She also condemned the Democrat-supported idea of providing free college to lower-income Americans, calling the proposal “a socialist takeover of higher education.”

“Now, depending on your personal politics, some of you might not find that notion as scary as I do,” DeVos said. “But mark my words: None of you would like the way it will work.”

The way the government has handled student loans was a case in point, she argued.

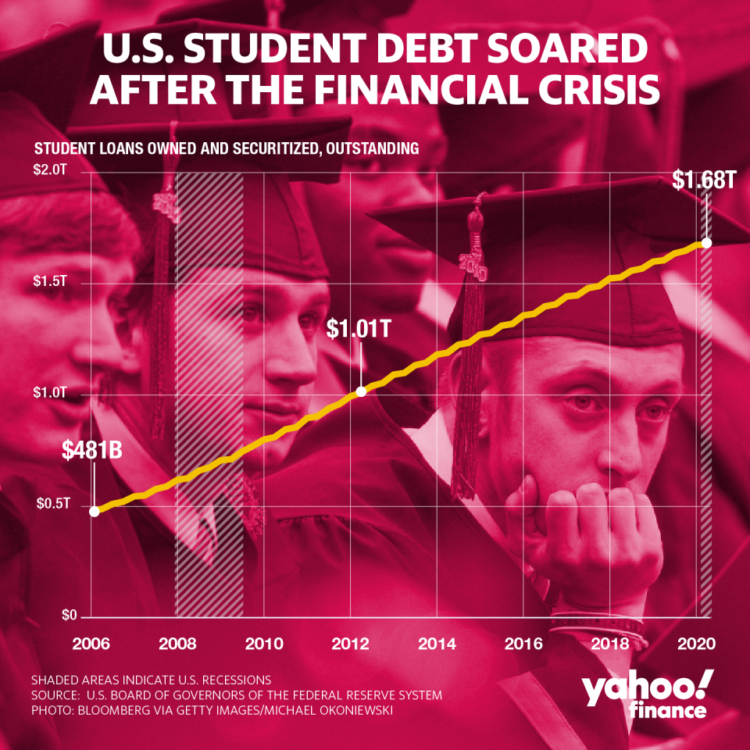

“The first step was monopolizing student lending,” DeVos said. “$1.5 trillion later, can anyone say with a straight face that students are better off? That taxpayers are better off?”

Making college free would water down the quality of American higher ed, DeVos claimed, adding: “If the politicians proposing ‘free college’ today get their way, just watch our colleges and universities begin to resemble a failing K-12 school, with the customer service of the DMV to boot.”

DeVos also asserted that it would be “fundamentally unfair to ask two-thirds of Americans who don’t go to college to pay the bills for the mere one-third who do. And it’s even more unfair to those who have held up their end of the bargain and paid back their student loans themselves to subsidize those who don’t save, plan, and pay.”

Instead, she proposed making FSA, which holds the trillion-dollar loan portfolio, a standalone government agency with its own Board of Governors.

“Today, FSA has more than $1.5 trillion in outstanding loans on the books,” DeVos noted. “Too many of those loans are either delinquent, in default, or are loans on which borrowers are paying so little [that] their loan balance continues to grow.”

‘It was a deeply inappropriate speech’

Reaction to her speech was both swift and sharp.

“It was a deeply inappropriate speech to be given at an apolitical training conference,” Eddy Conroy, associate director of institutional transformation at Temple University’s Hope Center College, Community, and Justice, told Yahoo Finance. “It was a nakedly political speech which is very on brand for Betsy DeVos…. [and] it also frankly feels very anti-higher education.”

Devos’ comments on forgiveness being “insidious” was also concerning, Conroy added: “I kind of am sort of gobsmacked by that. …. Fundamentally, this was a Secretary of Education who didn’t feel like students deserved much support of all. And this is just an extension of that general feeling.”

Betsy Mayotte, president of the Institute of Student Loan Advisors, told Yahoo Finance that the comments “show a real lack of understanding of what the average college student looks like and on the issue of the cost of higher education. It appears she has not spent her time as secretary studying the data and the issues but has instead chosen to hang her hat on partisan policy one liners.”

Mayotte added that to say loan forgiveness is not fair to those who paid off their loans is also a misunderstanding, as that is “assuming that the playing field is equal to begin with.”

Amid the largely political speech, DeVos mentioned one topic that everyone seems to agree on right now: The cost of higher education is becoming out of control.

“Institutions must also take a long look in the mirror,” DeVos said. “The higher education industry needs to deliver products that are worth the price tag.”

Mark Zuckerberg is facing some major financial consequences, according to Forbes, losing billions of dollars, as well as his No.5-richest man rank as users continue to be shut out of Facebook, Messenger, Instagram, and WhatsApp.

After mass complaints about the various platforms in the Facebook family being down, and users getting error messages when trying to log on, the company said it was working to resolve the issue.

With all four now off-air for several hours, Zuckerberg has faced a pile-on on rival social media platforms, and habitual Facebook users have taken to other apps that aren’t experiencing issues, such as Twitter and Telegram, to express their dissatisfaction. Many have even temporarily celebrated the absence of Facebook.

Facebook and Instagram go mysteriously offline and, for one shining day, the world becomes a healthier place. #facebookdown

— Edward Snowden (@Snowden) October 4, 2021

Zuckerberg has lost billions as a result of the outage, according to real-time tracking by Forbes. Its list of “today’s winners and losers” tracks from the close of business the previous day, meaning the CEO’s massive losses have clearly occurred since users began experiencing technical issues.

Other leaders in Big Tech have also seen recent losses, according to the data, with Amazon’s Jeff Bezos and Microsoft’s Bill Gates both losing billions, too, though those losses are still comparatively minor in the shadow of Zuckerberg’s $6.7 billion hit, as of the time of writing. The loss has put Zuckerberg at sixth on Forbes’ list of the world’s top billionaires, with Elon Musk at the zenith.

Facebook, WhatsApp & Instagram ALL down in major worldwide outage

Facebook stock has dropped multiple percentage points in the wake of not only the aforementioned technical difficulties, but also a ‘60 Minutes’ interview with a whistleblower from the company that aired on Sunday night.

Data scientist Frances Haugen came forward as the source of a recent report claiming the company had been aware of the negative effects its services could have on users, and its censorship ‘measures’ had been used to increase only its profits, rather than to fight misinformation, as it had claimed.

Haugen will appear before Congress this week for a hearing titled ‘Protecting Kids Online,’ which will focus on the alleged negative effects of Facebook’s algorithms on youths.

‘Betrayal of democracy’? Whistleblower blasts Facebook for prioritizing profits over fighting ‘hate speech & misinformation’

If you like this story, share it with a friend!

Global debt balloons to record highs

German military to sell tons of toilet paper

First female Saudi astronaut heads to space

Nigeria takes step to combat fuel shortages

US will default if debt deal fails – treasury secretary

Village People demand Trump stop using their music

Hollywood star pulls out of hosting awards show amid strike

Rock icon slams German authorities

Agatha Christie novels chopped by ‘sensitivity readers’ – media

Marvel star back in training after breaking over 30 bones

Turkish minister escapes fire blast (VIDEO)

Trump savages pop star’s Super Bowl performance

Alec Baldwin sued by Ukrainian family of slain cinematographer

Duran Duran stumbles, Dolly Parton rolls into Rock Hall

Sweden probes possible plot behind Russian pipeline leaks

Global debt balloons to record highs

It’s now $45 trillion higher than its pre-pandemic level and is expected to continue growing rapidly, a top trade body...

Nigeria takes step to combat fuel shortages

The West African country has built a giant oil refinery to cover domestic demand Nigeria will commission its new Dangote...

US will default if debt deal fails – treasury secretary

The current borrowing limit is a constraint on Washington’s ability to meet its obligations, Janet Yellen insists America’s chances of...

Facebook parent Meta fined €1.2 billion by Irish watchdog

The American tech company has been accused of violating EU data privacy rules US tech giant Meta has been hit...

UK’s business with sanctioned country booming

Trade between Britain and Iran has reached the highest level in a decade, according to official data, apparently having been...

Erdogan election defeat would be ‘revenge’ – Syrian Kurds

The YPG claims the Turkish president failing to win another term would be payback for Ankara’s counter-terrorism operations in Syria...

Chinese special envoy meets with Zelensky

Li Hui visited Kiev to share Beijing’s views on a political settlement to the Ukraine crisis Ukrainian President Vladimir Zelensky...

Pakistan’s top court orders release of former PM Imran Khan

Pakistan’s Supreme Court has ordered the release of former prime minister Imran Khan, whose arrest earlier this week triggered deadly...

Kamala Harris to run AI taskforce

The US vice president will ask AI execs to evaluate the safety and fairness of their models US Vice President...

Most Americans want to move on from Biden and Trump – poll

70% of respondents said the incumbent shouldn’t bid for office in 2024, with that figure 60% for the Republican former...

Disgraced ex-PM Liz Truss seeks to ruin any hopes for normal UK-China ties

The former premier’s Taiwan trip is nothing but a provocation for Beijing to lash out at London, sinking any constructive...

India facing challenge to steer SCO agenda away from Western-dominated frameworks

The Shanghai Cooperation Organisation is looking at ways to address the most pressing global issues without being a disruptive influence...

China isn’t the biggest threat to Italy’s prosperity

Rome is considering leaving the Belt and Road Initiative in a move which will place virtue signaling to other Western...

Meet the Czech lawyer who rallies thousands to shake up the EU establishment

In mid-April, a fledgling political party that recently formed in the Czech Republic called Pravo Respekt Odbornost (Law Respect Expertise;...

UK shows signs of good will to China, but it’s not the one calling the shots in this relationship

The British foreign secretary says antagonizing Beijing goes against London’s ‘national interests’, but Washington has other ideas British Foreign Secretary...

conic Smiths bassist dies aged 59

The bassist with legendary English rock band The Smiths, Andy Rourke, has died at the age of 59, the group’s...

Village People demand Trump stop using their music

A viral video emerged last week of Donald Trump dancing to a Village People song at his Florida estate Village...

Hollywood star pulls out of hosting awards show amid strike

Drew Barrymore is stepping down as host of this year’s MTV Movie & Music Awards, due to be held on...

Mexico condemns US ‘interference’ in drug war

The DEA’s infiltration of the Sinaloa Cartel without state permission amounts to espionage, the Mexican president says Mexican President Andres...

Rock icon slams German authorities

Pink Floyd co-founder Roger Waters criticized the city of Frankfurt for canceling his concert and vowed to take legal action...

-

TECHNOLOGY12 months ago

TECHNOLOGY12 months agoHow much YouTube pays for 1 million views, according to creators

-

FINANCE11 months ago

Facebook parent Meta fined €1.2 billion by Irish watchdog

-

LIFE12 months ago

Hollywood star pulls out of hosting awards show amid strike

-

LIFE11 months ago

conic Smiths bassist dies aged 59

-

NEWS11 months ago

NEWS11 months agoKenya supports creation of pan-African court

-

FINANCE11 months ago

US will default if debt deal fails – treasury secretary

-

FINANCE11 months ago

Global debt balloons to record highs

-

WAR11 months ago

WAR11 months agoUkraine won’t join NATO anytime soon – Scholz