INVESTMENTS

Coronavirus stimulus: Lawmakers unveil $908 billion bipartisan relief proposal

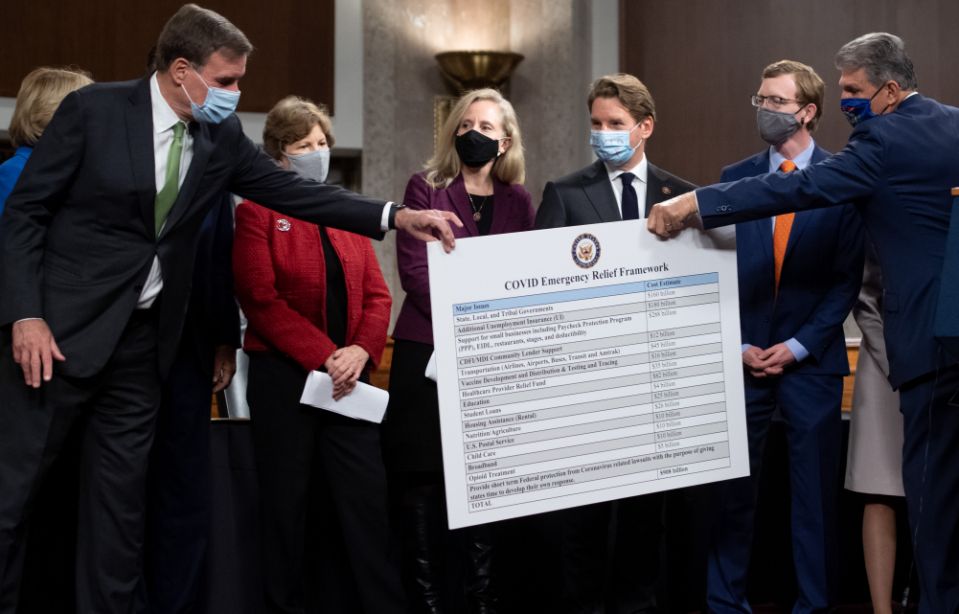

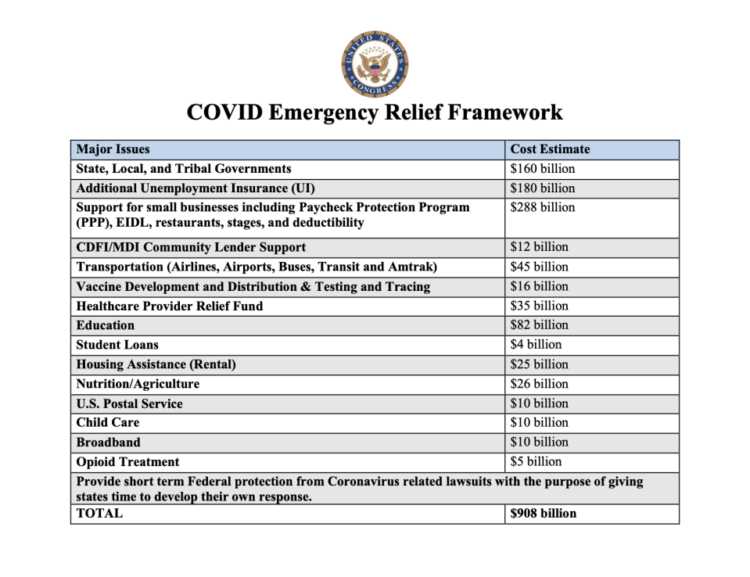

A group of Republican and Democratic lawmakers unveiled a $908 billion stimulus plan on Dec. 1, in an attempt to break through partisan gridlock after months of failed relief negotiations.

Lawmakers and the White House are facing growing pressure to pass additional coronavirus relief as COVID-19 cases surge, states and cities put more restrictions in place and existing relief programs soon expire.

“It’s not the time for political brinkmanship,” said Sen. Joe Manchin (D., W.V.) at a press conference on Tuesday.

The bipartisan group of lawmakers — including Manchin, Senators Mark Warner (D., Virg.), Bill Cassidy (R., La.), Susan Collins (R., Me.), Mitt Romney (R., Utah) and several others — say their plan aims to find common ground on some of the most pressing issues, and it could be used as a framework for the next stimulus package.

The compromise proposal, which totals $908 billion, includes $160 billion for state, local and tribal governments —a top priority for Democratic lawmakers, which most Republicans opposed — and short-term protections from coronavirus lawsuits, a “red line” for Republican Majority Leader Mitch McConnell that Democrats have rejected. Those two issues alone have caused significant problems throughout negotiations so far. Romney said the temporary protections give states time to put their own protections in place.

“Any state that doesn’t put in place protections hasn’t been thinking this through very carefully — because if I were a CEO I would never think of putting a new business in a state that didn’t have liability protection for COVID,” said Romney.

The proposal also includes $288 billion to support small businesses through the Paycheck Protection Program, Economic Injury and Disaster Loans and other provisions. The lawmakers are calling for $180 billion for additional unemployment insurance, which would provide a $300 weekly boost to jobless benefits. The extra $600 per week included in the CARES Act expired earlier this year.

The proposal also calls for funding for vaccine development and distribution, testing and tracing, education, child care, rental assistance, student loan assistance, transportation and more. The plan does not include another round of stimulus checks.

“Republicans and Democrats, neither of us got everything we wanted. Both of us got much of what we wanted. I think that combination reflects what Congress is supposed to do — Reconciling different priorities but ultimately doing something good for the American people,” said Cassidy.

The framework aims to provide relief through the first quarter of 2021, when President-elect Biden and the next Congress could decide what further measures are necessary.

“It would be stupidity on steroids if Congress left for Christmas without doing an interim package as a bridge,” said Warner.

Manchin said the lawmakers could put together an actual bill quickly, and he’s hopeful Congressional leadership would put that legislation on the floor for a vote. Senators said the group has presented some of its ideas to Treasury Secretary Steven Mnuchin and sought his input on necessary funding, but they told reporters they didn’t know if the White House would support the plan.

In a Senate Banking Committee hearing on Tuesday, Federal Reserve Chairman Jerome Powell and Mnuchin said they had not seen the specific details of the $908 billion proposal.

“It sounds like you’re hitting a lot of the areas that could definitely benefit from help and some of these are areas that are going to be experiencing a challenging winter,” said Powell.

Mnuchin said he spoke with Republican leaders in the House and Senate on Monday and President Trump on Tuesday morning.

“We all believe there should be targeted fiscal response,” Mnuchin said in the hearing.

Some lawmakers and experts are hoping to include some relief measures in a funding bill to avoid a government shutdown on Dec. 11. It’s still not clear whether or not that will happen.

In a separate attempt to push coronavirus relief forward, a group of 30 Democratic senators on Tuesday sent a letter to Senate leaders urging them to extend the programs in the next round of COVID-19 relief.

Majority Leader Mitch McConnell (R-Ky) rejected the proposal during a press conference on Tuesday afternoon.

“We just don’t have time to waste time,” said McConnell when asked about the compromise plan. “I think the way you make a law for sure, is you know you’ve got a presidential signature.”

The Majority Leader said he’s been in touch with White House officials about what President Trump would support, and he plans to offer proposals to GOP senators and get their feedback. McConnell said there needs to be a “targeted relief bill” before the end of the year, and suggested some measures would likely be included in a government funding bill.

Mark Zuckerberg is facing some major financial consequences, according to Forbes, losing billions of dollars, as well as his No.5-richest man rank as users continue to be shut out of Facebook, Messenger, Instagram, and WhatsApp.

After mass complaints about the various platforms in the Facebook family being down, and users getting error messages when trying to log on, the company said it was working to resolve the issue.

With all four now off-air for several hours, Zuckerberg has faced a pile-on on rival social media platforms, and habitual Facebook users have taken to other apps that aren’t experiencing issues, such as Twitter and Telegram, to express their dissatisfaction. Many have even temporarily celebrated the absence of Facebook.

Facebook and Instagram go mysteriously offline and, for one shining day, the world becomes a healthier place. #facebookdown

— Edward Snowden (@Snowden) October 4, 2021

Zuckerberg has lost billions as a result of the outage, according to real-time tracking by Forbes. Its list of “today’s winners and losers” tracks from the close of business the previous day, meaning the CEO’s massive losses have clearly occurred since users began experiencing technical issues.

Other leaders in Big Tech have also seen recent losses, according to the data, with Amazon’s Jeff Bezos and Microsoft’s Bill Gates both losing billions, too, though those losses are still comparatively minor in the shadow of Zuckerberg’s $6.7 billion hit, as of the time of writing. The loss has put Zuckerberg at sixth on Forbes’ list of the world’s top billionaires, with Elon Musk at the zenith.

Facebook, WhatsApp & Instagram ALL down in major worldwide outage

Facebook stock has dropped multiple percentage points in the wake of not only the aforementioned technical difficulties, but also a ‘60 Minutes’ interview with a whistleblower from the company that aired on Sunday night.

Data scientist Frances Haugen came forward as the source of a recent report claiming the company had been aware of the negative effects its services could have on users, and its censorship ‘measures’ had been used to increase only its profits, rather than to fight misinformation, as it had claimed.

Haugen will appear before Congress this week for a hearing titled ‘Protecting Kids Online,’ which will focus on the alleged negative effects of Facebook’s algorithms on youths.

‘Betrayal of democracy’? Whistleblower blasts Facebook for prioritizing profits over fighting ‘hate speech & misinformation’

If you like this story, share it with a friend!

Global debt balloons to record highs

German military to sell tons of toilet paper

First female Saudi astronaut heads to space

Nigeria takes step to combat fuel shortages

US will default if debt deal fails – treasury secretary

Village People demand Trump stop using their music

Hollywood star pulls out of hosting awards show amid strike

Rock icon slams German authorities

Agatha Christie novels chopped by ‘sensitivity readers’ – media

Marvel star back in training after breaking over 30 bones

Turkish minister escapes fire blast (VIDEO)

Trump savages pop star’s Super Bowl performance

Alec Baldwin sued by Ukrainian family of slain cinematographer

Duran Duran stumbles, Dolly Parton rolls into Rock Hall

Sweden probes possible plot behind Russian pipeline leaks

Global debt balloons to record highs

It’s now $45 trillion higher than its pre-pandemic level and is expected to continue growing rapidly, a top trade body...

Nigeria takes step to combat fuel shortages

The West African country has built a giant oil refinery to cover domestic demand Nigeria will commission its new Dangote...

US will default if debt deal fails – treasury secretary

The current borrowing limit is a constraint on Washington’s ability to meet its obligations, Janet Yellen insists America’s chances of...

Facebook parent Meta fined €1.2 billion by Irish watchdog

The American tech company has been accused of violating EU data privacy rules US tech giant Meta has been hit...

UK’s business with sanctioned country booming

Trade between Britain and Iran has reached the highest level in a decade, according to official data, apparently having been...

Erdogan election defeat would be ‘revenge’ – Syrian Kurds

The YPG claims the Turkish president failing to win another term would be payback for Ankara’s counter-terrorism operations in Syria...

Chinese special envoy meets with Zelensky

Li Hui visited Kiev to share Beijing’s views on a political settlement to the Ukraine crisis Ukrainian President Vladimir Zelensky...

Pakistan’s top court orders release of former PM Imran Khan

Pakistan’s Supreme Court has ordered the release of former prime minister Imran Khan, whose arrest earlier this week triggered deadly...

Kamala Harris to run AI taskforce

The US vice president will ask AI execs to evaluate the safety and fairness of their models US Vice President...

Most Americans want to move on from Biden and Trump – poll

70% of respondents said the incumbent shouldn’t bid for office in 2024, with that figure 60% for the Republican former...

Disgraced ex-PM Liz Truss seeks to ruin any hopes for normal UK-China ties

The former premier’s Taiwan trip is nothing but a provocation for Beijing to lash out at London, sinking any constructive...

India facing challenge to steer SCO agenda away from Western-dominated frameworks

The Shanghai Cooperation Organisation is looking at ways to address the most pressing global issues without being a disruptive influence...

China isn’t the biggest threat to Italy’s prosperity

Rome is considering leaving the Belt and Road Initiative in a move which will place virtue signaling to other Western...

Meet the Czech lawyer who rallies thousands to shake up the EU establishment

In mid-April, a fledgling political party that recently formed in the Czech Republic called Pravo Respekt Odbornost (Law Respect Expertise;...

UK shows signs of good will to China, but it’s not the one calling the shots in this relationship

The British foreign secretary says antagonizing Beijing goes against London’s ‘national interests’, but Washington has other ideas British Foreign Secretary...

conic Smiths bassist dies aged 59

The bassist with legendary English rock band The Smiths, Andy Rourke, has died at the age of 59, the group’s...

Village People demand Trump stop using their music

A viral video emerged last week of Donald Trump dancing to a Village People song at his Florida estate Village...

Hollywood star pulls out of hosting awards show amid strike

Drew Barrymore is stepping down as host of this year’s MTV Movie & Music Awards, due to be held on...

Mexico condemns US ‘interference’ in drug war

The DEA’s infiltration of the Sinaloa Cartel without state permission amounts to espionage, the Mexican president says Mexican President Andres...

Rock icon slams German authorities

Pink Floyd co-founder Roger Waters criticized the city of Frankfurt for canceling his concert and vowed to take legal action...

-

TECHNOLOGY12 months ago

TECHNOLOGY12 months agoHow much YouTube pays for 1 million views, according to creators

-

FINANCE11 months ago

Facebook parent Meta fined €1.2 billion by Irish watchdog

-

LIFE12 months ago

Hollywood star pulls out of hosting awards show amid strike

-

LIFE11 months ago

conic Smiths bassist dies aged 59

-

NEWS11 months ago

NEWS11 months agoKenya supports creation of pan-African court

-

FINANCE11 months ago

US will default if debt deal fails – treasury secretary

-

FINANCE11 months ago

Global debt balloons to record highs

-

WAR11 months ago

WAR11 months agoUkraine won’t join NATO anytime soon – Scholz